This is part seven in an ongoing series. Prior posts are available here.

In the last post, we noted that year-over-year growth rates had declined from the stimulus-bump highs but remained above growth from earlier in 2020. This post looks at GMV trends for the high-level categories through the first half of May to see if those trends continued.

As a reminder, because there are so many changes on a daily basis, we’ve built a COVID-19 resources page to help you keep up with major developments in e-commerce. This blog post is designed to provide an update on Rithum aggregate gross merchandise value (GMV) trends.

First, some important points to understand before digging into the data:

- This data is based on marketplaces GMV aggregated across our entire customer base globally and compares Jan 1 – May 16, 2019 against Jan 1 – May 15, 2020. The final dates are offset by one day due to leap year.

- The data presented below highlights only specific marketplace categories, which are merely a subset of all categories. Because marketplaces have different category structures, the data is presented using categories that have been standardized by Rithum.

- This data is not a proxy for overall e-commerce activity or the performance of any individual business, including Rithum or any individual marketplace.

- The data shown below is based on a year-over-year comparison of trailing 7-day GMV and is expressed as percentage growth, but with actual numbers removed. The Y-axis scale is different on each graph.

- All calculations are done in USD. Global currencies are converted to USD using the conversion rate on the day of the order. These results are not normalized to account for fluctuating exchange rates. Please note that there has been significant volatility in various currencies, such as GBP, which may impact these trends.

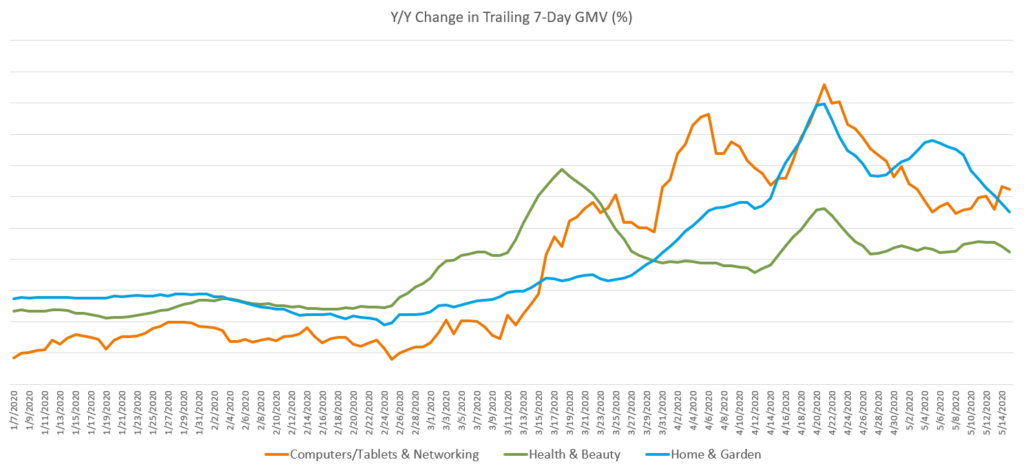

Even With the Stimulus Bump Behind Us, Growth Has Remained Elevated

Across the high-level categories we have been tracking, we have continued to see elevated growth in most of them. As noted in the last post, this growth declined from what we saw during the stimulus bump but has remained well above the year-over-year growth rates from early 2020.

Three top-level categories that we have consistently highlighted in this series include “computers/networking”, “health and beauty”, and “home and garden.” Year-over-year growth rates in all three of these categories were well above the growth rates from early 2020. Growth in “health and beauty” has remained in a tight range since late April while “computers/networking” has remained relatively steady since early May. As of May 15, the growth rates in “home and garden” have been declining from recent highs.

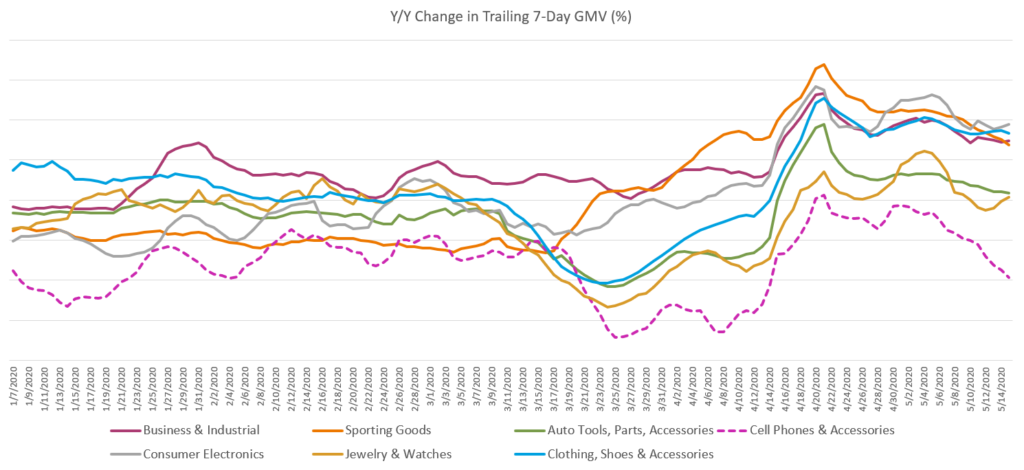

As with the categories illustrated above, the majority of the categories in the chart below had growth rates that experienced a gradual decline from the peak of the stimulus bump but that remain well above those of earlier in 2020. The two primary exceptions to this trend are the category of “jewelry/watches”, which had similar growth rates to early 2020 after recovering from the big dip that began in March, and “cell phones/accessories”, which appeared to be on its way to testing the lows of Q1. As of mid-May, the “auto tools/parts/accessories” category had growth rates that have recently declined but still remained in-line with the peak growth experienced in Q1.

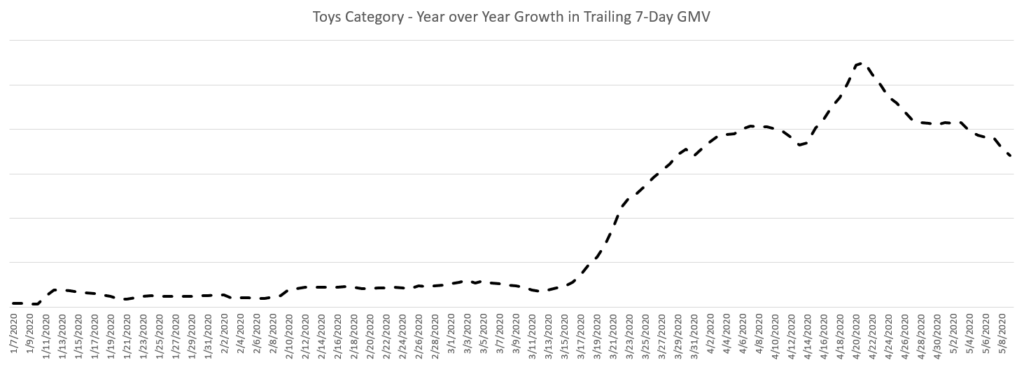

Toys

The toy category is one we have highlighted (see part 2) only in relation to some of the interesting subcategory growth we have seen during the pandemic, including outdoor bouncers and jigsaw puzzles. But this entire category has experienced growth, and we thought it would be worthwhile to take a deeper look into some of the other, larger subcategories. The data in this section is through May 9, 2020.

First, let’s take a look at the trend in growth rates of the overall toy category. From the chart below, it is apparent that year-over-year growth rates increased beginning in mid-March, around the same time as the US (and many other countries outside of Asia) began to get more serious about avoiding large crowds and social distancing. This is around the same time we started to see a divergence between the growth performance in essential/work-from-home categories and more discretionary categories. It seems that stocking up on kid-friendly activities during quarantine was deemed essential by consumers. As of May 9, growth remained elevated.

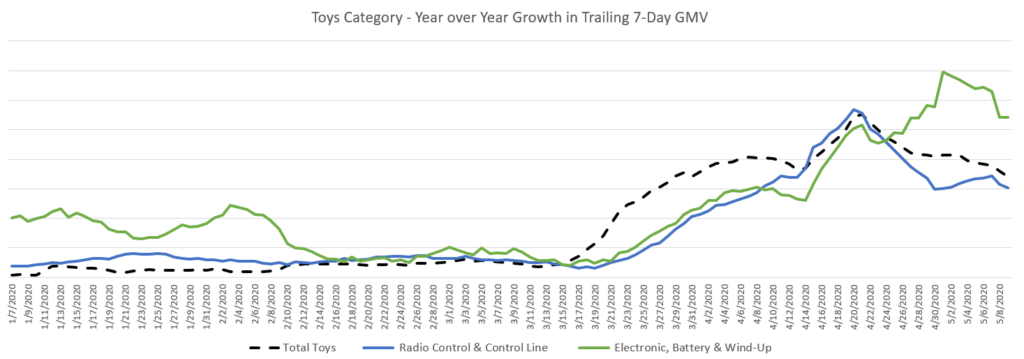

Radio control and electronic toys benefited roughly in-line with the overall category. Growth in electronic toys surpassed the overall category in late April and remained stronger through early May.

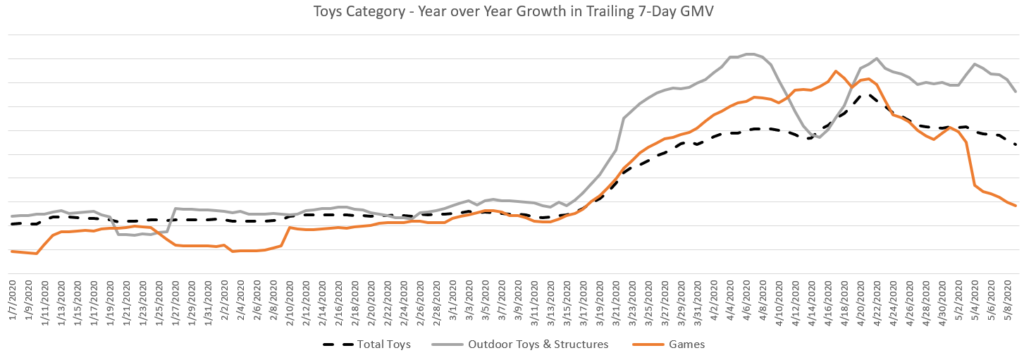

Growth in the “outdoor toys and structures” subcategory has exceeded the overall toy category since March, while the growth in “games” declined to levels just above those experienced earlier in 2020, perhaps due to the arrival of spring and all those new outdoor toys.

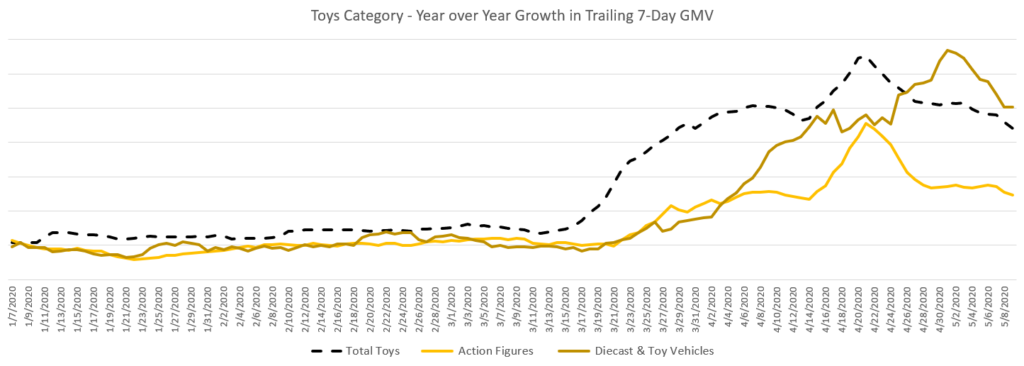

The subcategories of “action figures” and “diecast/toy vehicles” had similar growth rates through much of the first quarter, though “diecast/toy vehicles” had significantly higher growth in Q2 through the early part of May.

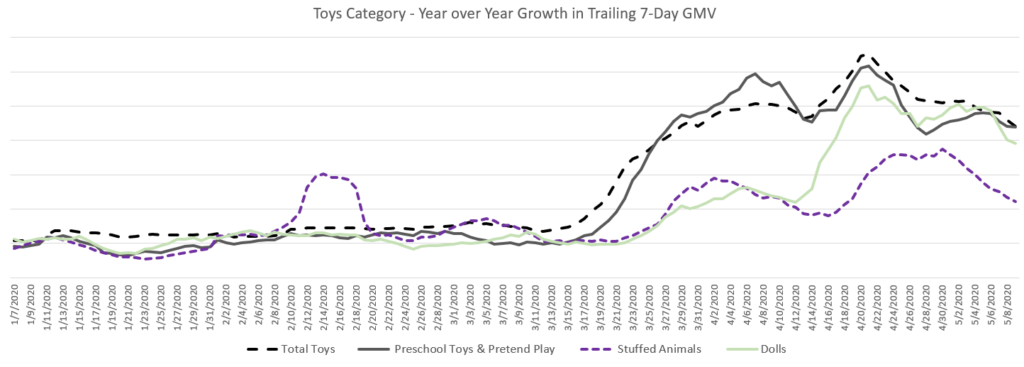

Growth in the subcategory of “preschool toys” largely mirrored that of the overall toy category through early May. The subcategories of “stuffed animals” and “dolls” have trailed the overall toy category for most of 2020, though “dolls” experienced a significant boost in mid-April that has continued.

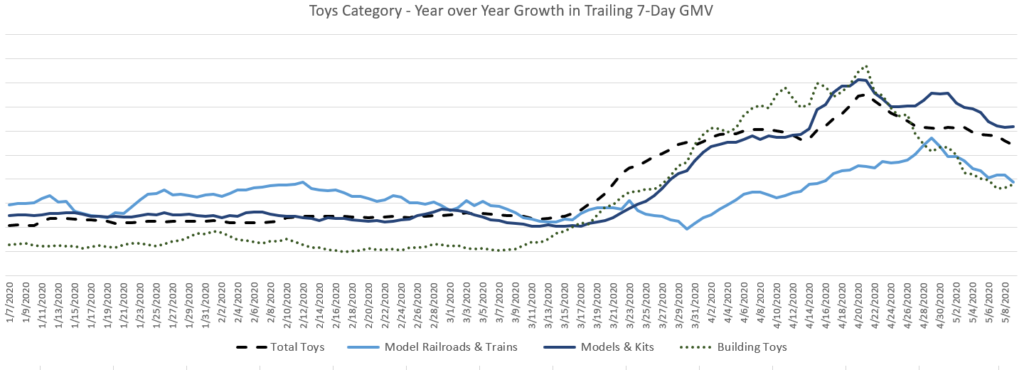

The “building toys” subcategory grew sharply from mid-March but has also experienced a sharper decline since mid-to-late April. Growth in “models and kits” followed roughly the same path but has declined at a much slower rate and remained well above earlier growth rates. Growth in “model railroads/trains” was more gradual and not as dramatic. From late April, this subcategory gradually declined, approaching the Q1 high mark set in mid-February.

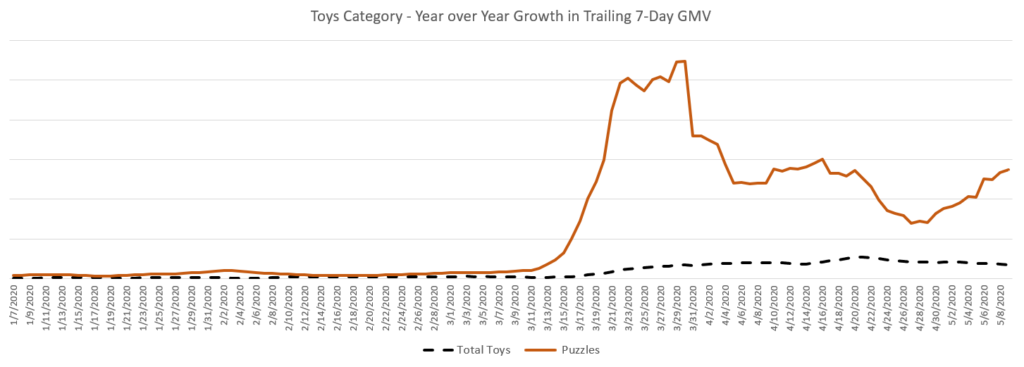

Finally, as we previously mentioned in part 2 of this series, “puzzles” experienced the most growth of any subcategory. The growth has been so dramatic that we need to plot it on its own graph. Growth in “puzzles” is well off the highs of late March, but it remains significant.

Conclusion

Growth rates continue to remain high across most of the major categories. With many nations and regions starting to implement opening plans, we’ll continue to follow marketplace trends to understand the impact on e-commerce.

In closing, we would like to reiterate from our blog last week that the COVID-19 pandemic has created extreme turmoil globally. The impact on supply and demand and the way people work is in the news daily and can be seen in the data above. The impact seems trivial relative to the personal toll. Nevertheless, the job of ensuring that food, medicine, and other essentials make their way to people globally is important to keep society functioning as normally as possible while we work our way through the current pandemic. So, in addition to thanking medical professionals, researchers, and others for their heroic efforts in treating the sick and trying to find a cure, we’d like to thank those of you in the factories, in the grocery stores, in the distribution centers, and in the delivery trucks helping to bring us the items we need to live.